The UAE’s move toward mandatory e-invoicing represents a structural transformation in how tax compliance is monitored, verified, and enforced. For years, VAT compliance relied largely on periodic tax return submissions, followed by retrospective audits conducted months, but that model is changing.

Under the new system, every eligible transaction will pass through a structured, standardized, and near real-time verification framework. The Federal Tax Authority (FTA) will gain significant visibility into invoice-level data, transforming invoices from routine accounting documents into compliance checkpoints.

For businesses operating complex group structures, whether formed through UAE freezone setup or UAE mainland setup, this new regime introduces a level of transparency that will expose inconsistencies, pricing irregularities, and governance gaps.

Entrepreneurs eyeing business setup in the UAE must understand the compliance standards and risks associated with UAE e-Invoicing and that’s what this blog post delves into.

Understanding the UAE E-Invoicing Framework

The UAE’s e-invoicing mandate primarily applies to:

- Business-to-Business (B2B) transactions

- Business-to-Government (B2G) transactions

All VAT-registered natural and legal persons issuing taxable supplies will be required to generate invoices in the prescribed PINT-AE format. Business-to-Consumer (B2C) transactions are currently outside the scope, with the focus placed on entity-level commercial activity. Key milestones include:

- Q4 2025: Accreditation of approved service providers

- January 2026: Pilot phase for selected sectors

- July 2026: Full mandatory implementation for B2B and B2G transactions

Once implemented, invoices will undergo structured verification before acceptance, reducing the opportunity for manipulation or retrospective correction. Investors seeking company formation in the UAE or those expanding through new entities, system integration and early preparation is critical.

From Periodic VAT Filing to Continuous Transaction Monitoring

Under the traditional VAT model:

- Returns are submitted monthly or quarterly

- Audits occur retrospectively

- Errors may remain undetected for extended periods

This time lag has historically allowed discrepancies to go unnoticed until formal audit intervention. With e-invoicing:

- Transactions are verified at the invoice level

- Data becomes available in real time

- Cross-checking between supplier and customer becomes immediate

- Pattern detection becomes automated

For group entities operating across UAE free zones and mainland jurisdictions, this real-time cross-verification introduces heightened scrutiny of intercompany flows.

What e-Invoicing Will Reveal About Group Structures?

1. Transfer Pricing & Related-Party Transactions

Intercompany management fees, service charges, and shared-cost allocations will become fully visible through structured invoice data. Where pricing deviates from arm’s-length standards, discrepancies may trigger scrutiny under both:

- UAE Corporate Tax rules

- VAT regulations

Entities established through UAE freezone setup arrangements, especially those benefiting from tax incentives, must ensure that intercompany pricing aligns with transfer pricing principles and documentation standards.

2. VAT Group Membership Inconsistencies

VAT grouping offers administrative efficiency, but improper implementation creates risk. E-invoicing will allow authorities to detect:

- Undeclared intra-group supplies

- Incorrect tax treatment within VAT groups

- Mismatches between entity activity and declared group membership

In complex structures formed through multiple UAE company formation stages, alignment between licensing, operational activity, and VAT registration must be reviewed carefully.

3. Permanent Establishment (PE) Exposure

Cross-border transactions will receive greater analytical scrutiny. Recurring invoices between UAE entities and foreign affiliates may signal:

- A fixed place of business

- Agency relationships

- Economic presence triggering PE status

Under Corporate Tax, the identification of a permanent establishment could result in the taxation of previously undeclared income within the UAE.

4. Duplicate or Artificial Transactions

Structured invoice validation can reveal:

- Duplicate billing patterns

- Circular transactions

- Unusual invoice sequencing

- Artificially inflated values

Patterns that may previously have gone unnoticed under manual audits will now be identifiable through system-level analytics.

5. Audit Quality: Before and After e-Invoicing

Before e-Invoicing:

- VAT audits were periodic

- Data was examined retrospectively

- Inconsistencies might surface long after the tax period

After e-Invoicing:

- Invoice-level scrutiny becomes immediate

- Discrepancies are flagged early

- Pattern-based risk analysis becomes automated

- Regulatory visibility expands significantly

This transition elevates the importance of internal controls, documentation discipline, and alignment between accounting systems and tax positions. Businesses that align early with e-invoicing standards will experience smoother regulatory interactions and greater strategic flexibility.

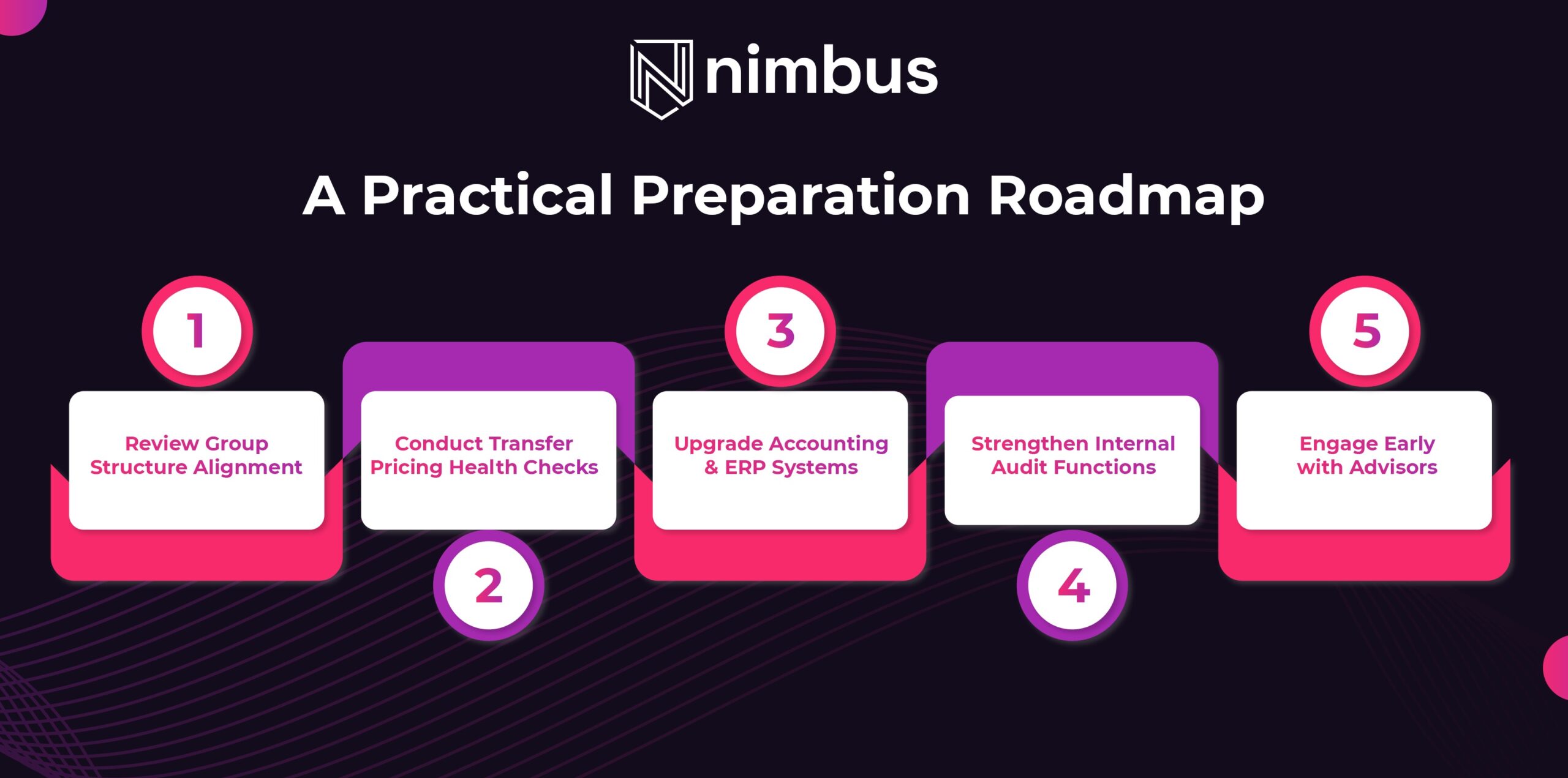

A Practical Preparation Roadmap

1. Review Group Structure Alignment

- Validate ownership chains

- Confirm licensing consistency

- Assess Free Zone eligibility under Corporate Tax

2. Conduct Transfer Pricing Health Checks

- Review intercompany pricing

- Update documentation

- Align policies with OECD standards

3. Upgrade Accounting & ERP Systems

- Ensure PINT-AE compatibility

- Integrate with accredited service providers

- Test real-time reporting capabilities

4. Strengthen Internal Audit Functions

- Shift from annual review to continuous compliance

- Perform invoice sampling and reconciliation

- Train finance teams on new verification processes

5. Engage Early with Advisors

Professional advisory support can identify structural risks before they become regulatory findings. For investors considering business setup in the UAE or restructuring, e-invoicing readiness should be embedded into future entity design.

The Bigger Picture: Transparency Is the New Standard

The UAE continues to evolve as a globally respected financial and commercial hub. With the introduction of Corporate Tax and now mandatory e-invoicing, regulatory sophistication is increasing in line with international standards. This shift enhances credibility on the global stage.

For businesses, however, it requires a cultural shift:

– From reactive filing → to proactive governance

– From annual audits → to continuous compliance

– From opaque structuring → to transparent alignment

The introduction of mandatory e-invoicing in 2026 marks a decisive move toward greater transparency and real-time regulatory oversight in the UAE.

Businesses that align systems, refine governance, and strengthen tax discipline today will not only avoid penalties, but will build stronger, more credible, and investor-ready organizations.